Retirement planning basics

Working with clients on a cohesive retirement strategy is a smoother process when you're fully prepared to speak to all the options. Our resources can help clarify the role of annuities and facilitate productive conversations.

Top 3 retirement planning benefits offered by annuities

If your clients aren't familiar with utilizing annuities as part of a retirement strategy, it can help to introduce them in terms of the key benefits they offer. You can easily turn these key retirement benefits into talking points:

Tax-deferred growth

Income options up to a lifetime

Guaranteed death benefit

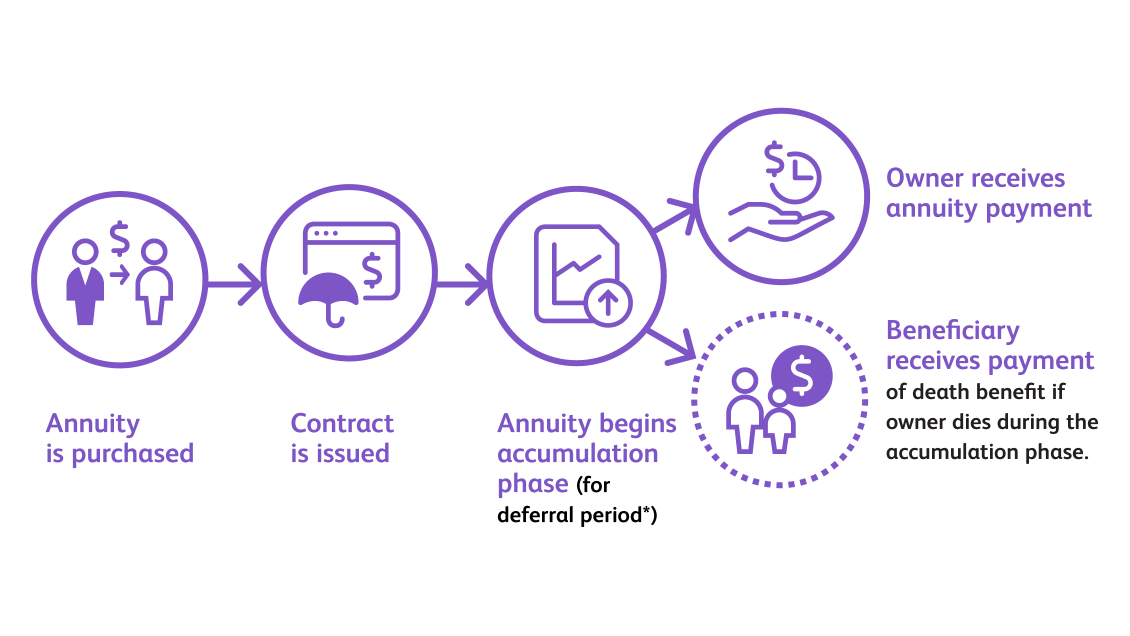

Explaining the 2 phases of annuities

Basic annuity designs: immediate or deferred?

There are two types of high-level annuity designs to consider, depending on client needs and retirement timing.

Explore different types of annuities

We offer different types of immediate and deferred annuities to better meet clients' various needs. Many of our annuities include enhanced income features, competitive fees and expanded investment options.

Compare features for the potential fit

Use this chart to help determine which type of annuity best meets clients’ retirement needs.

Tax-deferred growth

Death benefit

Options for single-payment purchase or installments

Minimum guaranteed interest rate

Principal protection

Indexed-linked growth potential

Immediate annuity

![]() *

*

Fixed annuity

Indexed annuity

Other related topics

Developing a holistic retirement plan

Key decisions in retirement planning

Why life insurance protects what matters to your clients

We’re here for you

We’re ready to help you deliver the protection and security your clients deserve. Reach out to us anytime for questions and support, and we’ll get in touch with you as soon as possible.

*Immediate annuities offer payout options that include survivor benefits.

Annuities are long-term insurance contracts intended for retirement planning. Annuities also may be subject to income tax and, if taken prior to age 59 ½, an additional 10% IRS tax penalty may apply. Because Protective and its representatives do not offer legal or tax advice, it is important that you talk with your own legal and tax advisor about your specific tax situation.

Indexed annuities are not an investment in any index, is not a security or stock market investment, does not participate in any stock or equity investment, and does not contain dividends.

WEB.3423234.12.21

To exercise your privacy choices,

To exercise your privacy choices,